Amid the rising cost of college and inflation, Massachusetts families say saving for college is a priority now more than ever, according to data from Fidelity Investments® and MEFA’s (Massachusetts Educational Financing Authority) 2024 College Savings Indicator Study. Nearly 8-in-10 Massachusetts parents have started saving in 2024 compared to 70% in 2018, and the majority (89%) agree the value of a college education is worth the cost. Even so, 32% aren’t sure what college will cost by the time their child enrolls and 41% use “their own best guess” to estimate costs.

Factors outside of parents’ control continue to weigh heavily on Massachusetts families’ minds. When it comes to saving for their child’s education, Massachusetts parents are most concerned about inflation and the rising costs of college (93%), followed by changes to education costs such as free tuition or student debt forgiveness (93%). Additionally, nearly 1-in-5 Massachusetts parents (18%) say credit card debt is the most significant barrier to their ability to save more for college expenses.

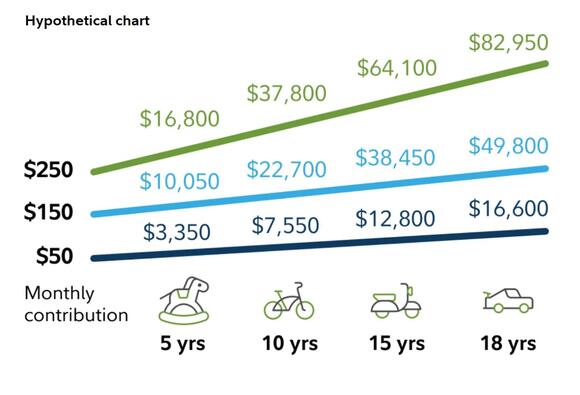

Massachusetts parents say that saving for college is their top priority. What’s more, nearly two-thirds (62%) of parents say they have a plan in place to reach their college savings goals. The vast majority (82%) say they’ll either continue their regular college savings contributions or even increase the amount of their regular contributions for the remainder of the year. Regular contributions, even when small, can accumulate over time and help ease the financial burden of rising costs.

MEFA, the state administrator for the U.Fund 529 College Investing Plan, provides a host of tools and resources at mefa.org to help families achieve their child’s education dreams. The U.Fund, the Commonwealth’s 529 -College Investing Plan, offers federal tax benefits and in-state tax deductions, and every child who is a Massachusetts resident is eligible to receive a $50 jump-start into a U.Fund account within one year of their birth or adoption thanks to the BabySteps Savings Plan.

“Saving for college remains a top priority for many Massachusetts families, and MEFA understands the challenges that parents are facing as the cost of living continues to rise,” said Thomas Graf, Executive Director of MEFA. “Though saving for the future may seem overwhelming right now, MEFA reminds families that even the smallest amount of college savings will make a difference over time. And MEFA’s college planning guidance and resources help families plan, save and pay for their child’s future.”

Massachusetts Parents Have High Expectations About Paying for College

As the total cost of college continues to rise, Massachusetts parents have high expectations when it comes to the amount they plan to pay for their child’s education. However, while Massachusetts parent’s may have high expectations, they’re still falling short on funding their intended college savings goal – an important step in long-term financial mobility. Massachusetts parents hope to pay for 61% of their child’s education, (down from 78% in 2022), but are only on track to meet 26% of that goal (down from 46% in 2022).

New Legislation Makes 529 Plans Even More Flexible

While many Massachusetts parents expect their child to attend some form of higher education, a sizeable 26% admit their child has expressed the possibility of not doing so – leaving many parents questioning the fate of their hard-earned 529 plan savings. Fortunately, new legislative changes may ease some of these concerns, as under certain conditions, 529 plan assets can now be transferred to a Roth IRA for the beneficiary – giving them a retirement boost. 1 The 529 account must be open for more than 15 years before being eligible for the rollover, which will be subject to annual Roth contribution limits and an aggregate lifetime limit of $35,000. In addition, the transfer amount must come from contributions made to the 529 account at least five years prior to the 529-to-Roth IRA transfer date. This new rule can help 529 account owners avoid taxes and penalties for withdrawals and can be particularly appealing for people looking to help their children get a head start on retirement.

Many ease some of these concerns, as under certain conditions, 529 plan assets can now be transferred to a Roth IRA for the beneficiary – giving them a retirement boost. 1 The 529 account must be open for more than 15 years before being eligible for the rollover, which will be subject to annual Roth contribution limits and an aggregate lifetime limit of $35,000. In addition, the transfer amount must come from contributions made to the 529 account at least five years prior to the 529-to-Roth IRA transfer date. This new rule can help 529 account owners avoid taxes and penalties for withdrawals and can be particularly appealing for people looking to help their children get a head start on retirement.

“Leveraging savings tools such as a 529 plan can make a substantial difference when it comes to easing the financial burden for college,” says Tony Durkan, vice president, head of 529 relationship management at Fidelity Investments. “Thanks to recent legislation like SECURE 2.0, 529 plans have become even more flexible and enticing as a savings vehicle for parents.”

The Importance of Having a Plan

While saving for college is a top priority among Massachusetts parents (and many have a plan for achieving college savings), more than one-third (38%) do not have a financial plan in place to meet their broader goals. As a financial services firm dedicated to helping people live better lives, Fidelity has a long-standing commitment to providing resources and education, to help the next generation make informed financial decisions. MEFA offers college planning resources across mefa.org2, including videos, blog posts, podcasts and calculators as well as college planning experts available to guide families through the entire college planning process.

Among those with children nearing college age, over half (53%) believe their child understands how much their total college education could cost, and the total potential amount of student loan debt they may incur, yet 27% have not discussed the total cost of college with their child and 39% have not discussed the amount of student debt that their child may incur following graduation. Two-thirds (66%) of parents agree that concerns about student loan debt is a motivating factor in saving for their child’s college education. Yet parents continue to underestimate the amount of student debt their child will incur. MEFA provides guidance to help families understand the cost of borrowing, and resources such as Exploring College Loans.

Should you be in the midst of a divorce or contemplating divorce, contact the Law Offices of Renee Lazar at 978-844-4095 to schedule a FREE one hour no obligation consultation.

fidelity.com